Fixed Income: the road ahead

In Short

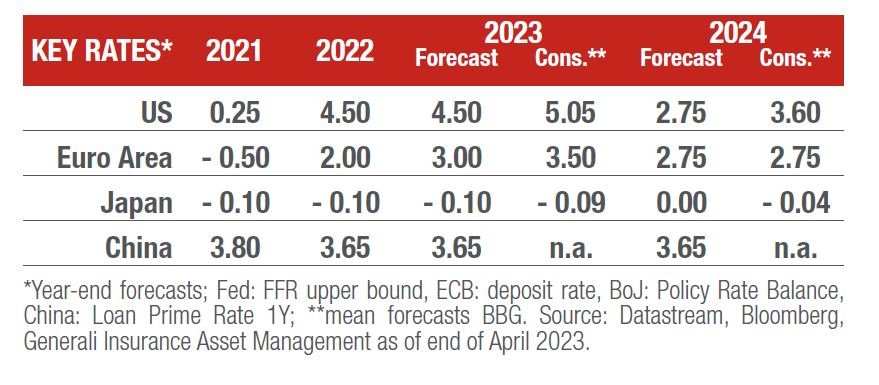

KEY DATA:

Rates forecasts vs consensus

Views from across the Generali Investments ecosystem

Recent crises within US regional banks and the more idiosyncratic case of Credit Suisse have various underlying causes. However, the overall context of these issues is undoubtedly the sudden and significant tightening of financial conditions in the past year.

In light of what continues to be a rollercoaster year for bond markets, we asked some of the fixed income portfolio managers around the Generali Investments ecosystem to answer this key question:

“Where are we in the RATE HIKING CYCLE, considering INFLATION on one side and the BANKING CRISIS on the other, and HOW ARE YOU POSITIONED FOR THE ROAD AHEAD?”

EUROPEAN GOVERNMENT BONDS AND CORPORATE CREDIT

Positioned for a lower rate volatility regime

MAURO VALLE

Head of Fixed Income and Fund Manager

After the turmoil in the banking system, the rate hiking cycle is likely nearing its end. The market has abruptly realized that higher rates can destabilize the financial system. Central banks now need to carefully manage this aspect of monetary policy, in addition to inflation, to prevent an economic recession.

The Fed and ECB are probably only 25 and 50 basis points away from their terminal rate, respectively. The question for the coming months is how long they will keep the official rates unchanged.

Our portfolios are managing duration between underweight and neutral in a tactical approach, anticipating that 10-year rates will move within a range in the next few months as bond markets wait for economic developments and changes in central bank attitudes. The yield curve should continue to stay inverted, but there is a risk of a steepening trend beginning in the next months.

These developments have implications for companies’ balance sheets and corporate bond spreads. Banks are reaching optimal levels of profitability given the new rate environment, and now they need to protect themselves from a possible spike in insolvencies. They will do this by tightening financing conditions and being more selective in providing lending to private and corporate borrowers.

Unlike in previous crises, most European banks are now better capitalized and benefit from elevated liquidity buffers, so they can withstand a period of moderate recession coupled with high inflation. The real estate sector may come under pressure, but it’s important to distinguish sound business models based on residential, logistics, and prime office locations that could attract investors and debt refinancing solutions. Therefore, for high-quality senior corporate bonds, we foresee a period dominated by carry in a lower rate volatility regime.

"The Fed and ECB are probably only 25 and 50 basis points away from their terminal rate, respectively"

EMERGING MARKET DEBT

A flight to quality in emerging markets

PETER MARBER

CIO of Emerging Markets and Fund Manager

The volatility in rates this year is unprecedented, with two-year US Treasury yields rallying from 4.42% to 4.10% in January, only to leap to 5.07% by March 7th in the wake of Fed Chairman Powell’s hawkish messaging on inflation. However, anxieties piled on that week with news of Silicon Valley Bank’s collapse and Credit Suisse’s demise, sending 2-year yields to 3.76% on fears of bank system contagion. As fears faded, yields have backed-up to 4.17% as of April 18th.

Intraday volatility, too, has been off-the-charts high, making it easy to be whipsawed in the markets. Amid this craziness, we are trying to stay close to our benchmark in duration while also trying to keep credit quality high – at benchmark level or even better.

Emerging markets have seen a flight to quality, and this may continue through 2023, particularly if developed economies slow down due to rising.

“We are trying to stay close to our benchmarkin duration while also trying to keep credit quality high”

GLOBAL LONG-SHORT CORPORATE CREDIT

Wait for a rally to build negative convexity

SIMON THORP

CIO of Corporate Credit and Fund Manager

Our base case is that we are close to the top of rates in developed market countries. We expect inflation to continue to fall due to base effects but to remain around 4% in the US and 5-6% in Europe. We foresee developed economies on both sides of the Atlantic to weaken by the end of Q3 as credit tightening increases the already severe pressure on corporates and consumers.

The banking crisis will likely continue to “bubble” but will be replaced with some other problem(s) that will emerge as a direct result of recent economic policy extremes – most likely in the commercial or residential real estate sectors.

We expect heightened uncertainty, elevated volatility, credit spread de-compression, and rising global geo-political risk ahead. We have reduced credit risk, are looking to add duration risk, and will build negative convexity into the portfolio on any further rally from here with the goal of making profits from future spread widening.

"The banking crisis will likely continue to bubble"

TOTAL RETURN GLOBAL MULTI-STRATEGY

Staying invested in high quality credit and the short end of the curve

MAURO RATTO

Co-Founder and Co-Chief Investment Officer

We are getting closer to the end of the tightening cycle. However, resilient and sticky inflation could limit the room for manoeuvre of several central banks. Investors should also keep in mind that we are, perhaps, at the end of an economic cycle.

The US banking crisis, with the sector being less regulated than in Europe and with a strong presence of regional listed banks, will have several consequences, such as further tightening of credit conditions. Although markets may get excited about the potential end of the rate cycle, the still-high risk of inflation suggests that central banks will continue to cautiously complete the hiking process over the next 3-4 months, raising rates by 25 basis points, taking it up to 5.5/5.25%.

The inverted yield curve calls for caution in taking advantage of the end of the rate cycle. We see value particularly on the short end of the sovereign debt curve, where two-year rates at 5% are a fairly unique opportunity in my view.

Short term corporate bonds also present value and should continue to be very attractive in the coming months given tighter credit conditions caused by the US banking turmoil may further widen spreads.

In our portfolios, we are focusing on high quality investments given the willingness of banks to lend is being challenged by market instability. We are finding good risk-reward opportunities in selective investment grade BBB credits where we have done our homework and conducted thorough credit analysis, as well as in the crossover space where selective high quality high yield-investment grade opportunities can fly under the radar.

Overall, we believe investment grade is the place to be right now. Staying invested in very high quality securities is a prudent approach, as it may become more difficult for lower quality companies to finance their positions. We are avoiding companies that have to refinance a large portion of their debt stock in the next 12-18 months.

"The inverted yield curve calls for caution in taking advantage of the end of the rate cycle"

SOCIALLY RESPONSIBLE CREDIT

Mitigating credit risk with rigorous SRI analysis

STANISLAS DE BAILLIENCOURT

Head of Investment Management and Fund Manager

I believe that we are almost there in terms of the hiking cycle, with perhaps one more rate hike in the US and probably two in the eurozone, but small ones like 25 basis points.

The US regional banking crisis is one of the first, very visible examples of the impact of the aggressive hiking cycle of the past 12 months, so central banks are watching it very closely. Typically in the US, there is competition for banking deposits between money market funds and banks. If the Fed keeps hiking, it becomes even more complicated or more costly for banks to attract deposits. All in all, economic growth is still there but is levelling off. The banking situation is more of a US problem because of less regulation, especially for non-systemic banks.

In terms of opportunities, after a decade of the low rate environment, we are finally seeing attractive yields again. It’s also true that the yield curve is significantly inverted, especially Europe. In our responsible European credit portfolios, we like the mid-portion of the curve, which is less impacted by the inversion and offers quite high yields and interesting value. We favour short-dated bonds between two years and five years maturity and prefer quality intermediate credit, such as crossover BB ratings, which offer interesting value.

As investors focusing on socially responsible (SRI) credit, we have a ten-year track record in European SRI crossover credit, and we believe that an SRI approach is a powerful way to mitigate risk. The rigorous analysis of extra-financial criteria that we perform on potential credit investments allows us to more deeply understand the multiple sources of risk embedded in corporates. As well as avoiding key risks, we also aim to improve two key SRI metrics: the environmental impact of our portfolios and the job creation generated by investee companies.

Despite all the exceptional shocks to the economy during the last few years, economies and companies have proven to be quite resilient. Therefore, we believe that when credit spreads are as attractive as they are today, it’s an opportune time to take advantage of having some credit exposure, particularly selecting opportunities in investment grade and high yield SRI credit.

"We favour short-dated bonds between two years and five years maturity and prefer quality credit, such as crossover BB"